.png)

.png)

.png)

.png)

Return on Equity (ROE) - Definition, Formula, & Examples

Return on Equity (ROE) is a crucial financial ratio that measures a company's ability to generate net profit from each dollar of equity investment by shareholders.

ROE assesses how efficiently a company uses its equity capital to generate income. Understanding it is essential for evaluating a company's financial health and its ability to make profits from shareholder's equity.

Let’s learn more about ROE and its importance to the success of an enterprise.

What is Return on Equity?

Return on Equity (ROE) helps assess how efficiently a company uses its shareholders' equity capital to generate net income. The ROE formula is straightforward: it divides net income by average shareholders' equity.

Here’s the equation for calculating ROE:

Return on Equity (ROE) = Net Income / Average Shareholder's Equity

The result is expressed as a percentage.

Net Income Calculation: Net income is determined by subtracting all expenses, including interest and taxes, from net revenue.

Conservative Measurement: ROE is a conservative metric, deducting more expenses than other profitability measures like gross income or operating income.

For example, if a company has a net income of $200,000 and an average shareholder's equity of $1,000,000, the ROE would be 20%. That means for every dollar of shareholder’s equity, the company generates 20 cents in profit.

At the accounting cycle end, the ROE is recalculated to assess the company's performance. If the net profit margin rises or the equity base decreases, the ROE will increase, indicating a more efficient use of equity capital.

How to calculate Return on Equity

ROE represents the net profit margin that a company produces for its shareholders. You need to collect some critical financial figures to calculate ROE. These figures can be found in a company's end-of-year financial statements, specifically the income statement and balance sheet.

1. Determine Net Income

Net income is the amount of total revenue that remains after subtracting all costs, expenses, taxes, and preferred stock dividends. It's usually found at the end of a company's income statement.

Here’s how you can find net income:

- First, locate the company's total revenue on the income statement.

- Next, find the total expenses, which include the cost of goods sold, selling, general and administrative expenses, operating expenses, depreciation, interest, taxes, and any other costs.

- Subtract the total expenses from the total revenue. The result is the net income.

The equation for calculating Net Income is:

Net Income = Total Revenue - Total Expenses

2. Calculate Average Shareholders' Equity

Average Shareholder's Equity is calculated by adding the stockholders' equity at the beginning of a period to the equity at the end of the period and then dividing by two. This data can be found on the company's balance sheet.

Here are the steps to calculate the average shareholder's equity:

- First, find the shareholder's equity at the beginning of the period on the balance sheet.

- Next, locate the shareholder's equity at the end of the period.

- Add these two amounts together.

- Divide the sum by two to get the average shareholder's equity.

The equation for calculating Average Shareholder's Equity is:

Average Shareholder's Equity = (Beginning Shareholder's Equity + Ending Shareholder's Equity) / 2

3. Calculate Return on Equity

Now that you have both the net income and the average shareholder's equity, you can calculate the ROE. Divide the net income by the average shareholder's equity.

Here’s how to calculate ROE:

- Take the net income calculated earlier.

- Divide it by the average shareholder's equity you also calculated earlier.

- The result is the return on equity.

The equation for calculating Return on Equity is:

Return on Equity (ROE) = Net Income / Average Shareholder's Equity

Remember, ROE is expressed as a percentage.

ROE calculation examples

Let's look at a few examples to understand better how to calculate Return on Equity.

Here are a few examples of Return on Equity (ROE) calculations for fictional companies:

Example 1: Company A:

- Net Income: $1,000,000

- Shareholders' Equity: $5,000,000

ROE = (Net Income / Shareholders' Equity) × 100 ROE = ($1,000,000 / $5,000,000) × 100 ROE = 20%

In this example, Company A has an ROE of 20%, indicating that for every dollar of equity contributed by shareholders, the company generates a 20% return in net income.

Example 2: Company B:

- Net Income: $500,000

- Shareholders' Equity: $10,000,000

ROE = (Net Income / Shareholders' Equity) × 100 ROE = ($500,000 / $10,000,000) × 100 ROE = 5%

Here, Company B has an ROE of 5%, signifying a 5% return on equity capital.

Example 3: Company C:

- Net Income: $1,500,000

- Shareholders' Equity: $7,500,000

ROE = (Net Income / Shareholders' Equity) × 100 ROE = ($1,500,000 / $7,500,000) × 100 ROE = 20%

In this case, Company C also has an ROE of 20%, similar to Company A. Both companies generate a 20% return on equity, but their actual net incomes and equity levels differ.

These examples show how ROE is calculated by dividing net income by shareholders' equity and expressing the result as a percentage.

Interpreting Return on Equity

Interpreting the Return on Equity (ROE) is crucial for investors and analysts when evaluating a company's financial performance. The ROE tells us how effectively a company uses its equity to generate profits.

Here's how you can interpret ROE:

High ROE

An ROE above 15-20% is considered high and indicates that the company is efficiently using its shareholders' equity to generate profits. This is a positive sign for investors, as it shows that the company can generate a good return on the money that shareholders have invested.

Average ROE

An average ROE usually falls between 10-15%. This suggests that the company is generating an acceptable return on equity but may not be as efficient in using its equity as companies with a higher ROE.

Low ROE

An ROE below 10% is generally considered low and may indicate that the company is not effectively using its equity to generate profits. This can be a red flag for investors, as it suggests that the company may not be profitable or struggling to grow its earnings.

Please note that these are general guidelines, and ROE can vary significantly across different industries. Therefore, it's important to compare a company's ROE with the industry average or with its competitors for a more accurate assessment.

It is always best not to analyze ROE as an isolated metric. It should be seen in conjunction with other factors like industry benchmarks, cash flow analysis, historical company performance, and the overall financial health of the organization. One-time events and management decisions, such as stock buybacks or dividends, can influence ROE.

Comparing a company's ROE to industry peers provides context and helps determine its relative performance. To effectively analyze the trajectory of ROE over time, one practical approach is to construct a trend chart or graph.

This visual representation simplifies the detection of upward or downward trends in your company's ROE ratio. Moreover, it permits a side-by-side comparison of your company's ROE with industry benchmarks, offering insights into its performance relative to its peers.

Tracking ROE over time reveals its consistency and ability to generate profits. When assessing ROE trends over time, it becomes crucial to scrutinize for notable shifts or variations. A persistent and unwavering ROE signifies the efficient utilization of equity capital in profit generation for the company. Conversely, if ROE displays fluctuations or descends, it may signal underlying concerns demanding attention.

Additionally, it's valuable to examine related financial metrics like Return on Assets (ROA), Profit Margin, Asset Turnover, Financial Leverage, and the DuPont Formula for a comprehensive assessment of a company's financial performance:

- Return on Assets (ROA): Evaluates the efficiency of a company in using its assets to generate profits.

- Profit Margin: Computes the portion of revenue that converts into net income as a percentage.

- Asset Turnover: Measures the effectiveness of a company in leveraging its assets to generate sales.

- Financial Leverage: Examines how much a company employs debt to fund its operations.

- DuPont Formula: A comprehensive mathematical formula that dissects return on equity into its constituent components.

One-time events or discretionary management decisions, such as stock buybacks or dividend issuance, can impact the ROE ratio. By analyzing ROE over some time, you can assess your company's consistent performance and identify any trends or anomalies. This long-term analysis will provide valuable insights into the effectiveness of your business in generating profits for shareholders.

Limitations of ROE

While Return on Equity (ROE) can provide valuable insights into a company's profitability and efficiency, it also has its limitations and should be used cautiously:

1. Misleading ROE due to high debt levels

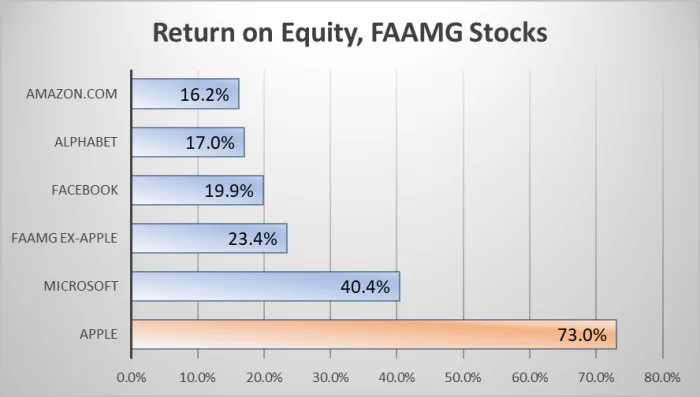

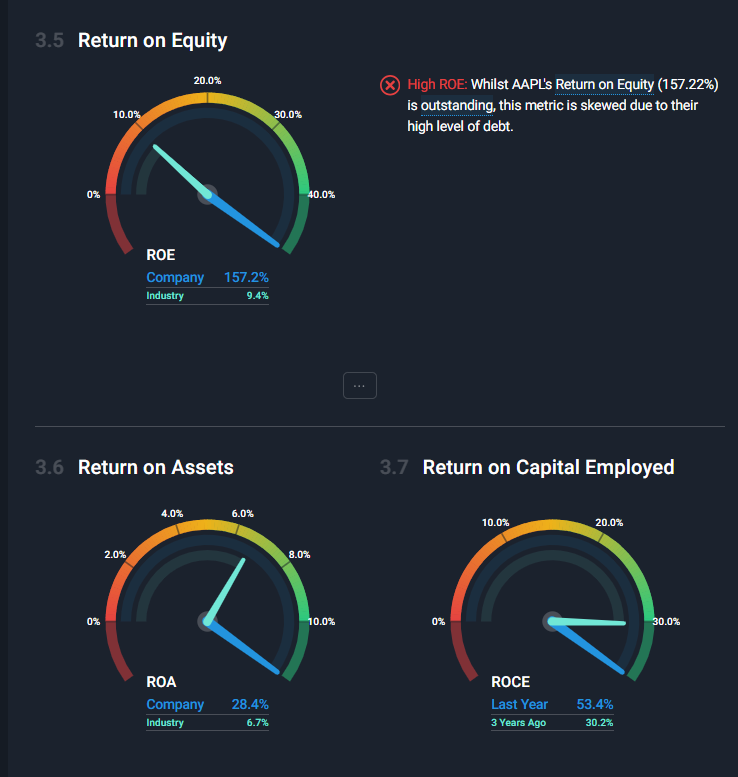

A company with high levels of debt might present a misleadingly high ROE. This is because the borrowed money increases the company's net income, which, in turn, inflates the ROE. However, this higher ROE does not necessarily mean that the company is efficiently using its equity. Instead, it may be exposing itself to higher levels of risk due to the increased debt.

2. ROE does not reflect the quality of earnings

ROE does not differentiate between earnings generated from sustainable business operations and those derived from one-time or non-recurring activities. Therefore, a high ROE could result from unusual or short-term profits, which may not be sustainable in the long term.

3. Not suitable for comparing companies across different industries

ROE is not always ideal for comparing companies across various sectors, as industry norms and average ROEs vary significantly. For example, a company in the tech industry may have a higher ROE compared to a company in the manufacturing industry due to differences in its operational structures and capital requirements.

4. Inflated ROE due to one-time gains

ROE may be inflated due to one-time gains such as the sale of an asset. While this might increase the net income and, thus, the ROE in the short term, it does not necessarily reflect the company's ability to generate profits consistently.

5. ROE does not account for future business prospects

ROE is a backward-looking metric that reflects past performance. It does not consider a company's future business prospects or growth potential. Therefore, it may not always provide a complete picture of a company's financial health or long-term profitability.

6. Dependence on management decisions

Management decisions, like issuing new shares or repurchasing existing ones, can affect ROE. A company might boost its ROE by buying back shares, thereby reducing equity. While this can temporarily increase ROE, it may not necessarily indicate an improvement in the company's operational efficiency or profitability.

Using the DuPont Formula

The DuPont Formula is a powerful analytical tool that allows us to break down ROE into its essential components, revealing the factors that shape a company's financial performance.

Here's a closer look at how DuPont analysis works:

- Profit margin: The first key component is the profit margin. This aspect assesses the company's efficiency in converting sales revenue into profits. A higher profit margin indicates that the company excels at generating earnings from its core operations.

- Asset turnover: Moving on to asset management, the total asset turnover is examined. This element gauges how effectively the company utilizes its assets to generate revenue. A higher asset turnover reflects efficient asset utilization. However, it's worth noting that companies with high turnover often have lower profit margins because they prioritize rapid sales over high profit margins.

- Financial leverage: The final piece of the puzzle is financial leverage, determined by the equity multiplier. This component delves into the strategic use of debt. By taking on more debt, a company can potentially amplify its ROE. However, this strategy introduces increased risk, as higher debt levels bring both potential rewards and potential risks.

Bringing these elements together, the DuPont Formula combines them in a straightforward manner:

ROE = Profit Margin x Asset Turnover x Financial Leverage

This formula provides us with a comprehensive view of a company's profitability. By breaking down ROE into these fundamental elements, we can better understand the sources of a company's profitability and assess its financial health in a more nuanced way.

Let's take a hypothetical example to illustrate this. Suppose a company has a profit margin of 5%, an asset turnover of 2 times, and a financial leverage 1.5. Using the DuPont Formula:

ROE = 5% x 2 x 1.5 = 15%

Based on DuPont analysis, this company's ROE is 15%. This indicates that for every dollar of equity, the company generates 15 cents of net income. This deeper insight into the company's operations and financial efficiency allows us to draw more accurate conclusions about its profitability and potential for future success.

Comparing various performance measures

Various metrics like Return on Equity (ROE), Return on Assets (ROA), Return on Capital Employed, and Return on Invested Capital (ROIC) are used to assess and compare the financial performance of different companies.

These metrics provide valuable insights into a company's efficiency, profitability, and overall financial health, allowing investors and analysts to make informed decisions.

Here's a breakdown of how these metrics differ and what questions they help answer:

1. Return on Equity (ROE)

- Key Question: How efficiently does a company utilize shareholder equity to generate after-tax profit (Net Income)?

- Calculation: ROE = (Net Income / Shareholders' Equity) × 100

- Use Case: ROE measures a company's ability to deliver returns to its equity shareholders. A high ROE suggests efficient utilization of equity capital.

2. Return on Assets (ROA)

- Key Question: How effectively does a company employ its total assets to generate after-tax profit (Net Income)?

- Calculation: ROA = (Net Income / Total Assets) × 100

- Use Case: ROA evaluates a company's asset efficiency. A higher ROA indicates efficient use of assets to generate profits.

3. Return on Capital Employed (ROCE)

- Key Question: How well does a company use its capital employed (both debt and equity) to generate pre-tax profit (EBIT)?

- Calculation: ROCE = (EBIT / Capital Employed) × 100

- Use Case: ROCE assesses a company's profitability and capital efficiency. A higher ROCE suggests that a company uses capital efficiently to generate profits.

4. Return on Invested Capital (ROIC)

- Key Question: How much after-tax profit (Net Income) does a company generate for all its investors, considering both equity and debt capital?

- Calculation: ROIC = (Net Income / (Total Equity + Total Debt)) × 100

- Use Case: ROIC offers a comprehensive view of a company's capital efficiency. It considers both equity and debt, making it a valuable metric for evaluating a company's overall financial performance.

These metrics serve distinct purposes and provide different angles for evaluating companies:

- ROE focuses on shareholder equity, making it particularly useful for assessing a company's return on shareholders' investments.

- ROA provides insights into how efficiently a company uses its assets to generate profits, regardless of its capital structure.

- ROCE helps compare the profitability of companies with different capital structures, as it considers both debt and equity.

- ROIC offers a broader perspective by considering both equity and debt capital, making it valuable for assessing a company's overall ability to generate returns for all its investors.

By comparing these metrics for different companies within the same industry or over time, investors and analysts can pinpoint strengths and weaknesses, identify areas for improvement, and make informed investment decisions. Ultimately, these performance measures help answer critical questions about a company's financial performance and its attractiveness to investors.

Using ROE to evaluate financial performance

Return on Equity (ROE) is a critical financial metric, essential for investors, analysts, and businesses.

Here's why ROE matters:

1. Profitability assessment: ROE measures how well a company generates profits relative to shareholders' equity. A high ROE means efficient use of investor capital and indicates a profitable business, making it an attractive investment.

2. Management competence: A consistently high ROE signals effective management. It shows that the management team makes smart decisions, utilizing investments wisely. This suggests they allocate resources well and plan strategically to maximize shareholder wealth.

3. Financial health check: ROE offers insight into a company's financial strength and sustainability. A stable ROE reflects a solid financial foundation, reassuring investors and indicating a lower-risk investment.

For investors, ROE matters because:

- It indicates if a company efficiently converts equity into earnings, a key profitability indicator.

- It reveals how effectively a company's leadership uses shareholder funds to make profits.

- Companies with high ROE often have room for growth as they can reinvest earnings.

- ROE lets you compare companies in the same industry, helping identify efficient performers.

- When used with other metrics, ROE guides investment decisions. A high, stable ROE suggests an attractive investment, while a declining ROE may signal problems.

- Low or negative ROE can flag financial troubles or inefficiencies.

- Tracking ROE over time helps assess a company's future prospects. A consistent increase suggests a positive outlook.

Factors impacting Return on Equity

Return on Equity (ROE) is susceptible to external and internal factors that can significantly influence its value. These factors are instrumental in understanding the dynamics of a company's profitability:

- Management changes: A new management team can inject fresh perspectives, innovative strategies, and improved operational efficiency, potentially leading to increased profits and ROE. Conversely, ineffective leadership can hinder performance.

- Market conditions: The broader market environment plays a pivotal role. In prosperous times, robust market performance can bolster a company's revenues and profitability, subsequently boosting ROE. Conversely, during market downturns, a decline in demand or increased competition can pressure profits and ROE.

- Economic conditions: The overall economic climate is a pivotal factor. A thriving economy can stimulate consumer spending and business investments, resulting in higher profits and ROE. Conversely, economic recessions or downturns can depress revenues and profitability, negatively impacting ROE.

- Capital structure: Changes in a company's capital structure, such as raising additional capital through equity or debt, can affect ROE. Successful capital infusion can fuel growth and enhance profitability, while difficulty securing capital can limit growth potential and ROE.

- Industry dynamics: The nature of the industry itself can significantly influence ROE. Factors such as industry profitability, competition levels, and barriers to entry can determine a company's ability to generate profits. In highly competitive sectors with low barriers to entry, companies may struggle to maintain high ROE. Conversely, industries with high profitability and substantial barriers to entry may provide more favorable conditions for ROE.

- Company size: The size of a company can also impact ROE. Larger, more established companies may have economies of scale, more resources, and a broad customer base that can contribute to higher ROE. However, smaller companies can also achieve high ROE if they have unique competitive advantages or operate in niche markets with less competition.

- Legal and regulatory changes: Laws and regulations can profoundly affect a company's profitability and, consequently, its ROE. For example, new tax laws could affect a company's net income, while changes in industry regulations could impact operational costs and revenues.

- Operational efficiency: A company’s ability to manage its resources effectively can significantly influence ROE. Efficient operations can lead to cost savings, higher margins, and increased profitability, boosting ROE. On the other hand, inefficiencies can lead to unnecessary expenses, lower margins, and decreased profitability, negatively affecting ROE.

- Financial leverage: The extent to which a company uses borrowed funds to finance its operations can impact ROE. Higher leverage can boost ROE if a company can generate more profits from the borrowed funds than the interest cost. However, excessive leverage can be risky and potentially lead to financial distress, negatively impacting ROE.

- Dividend policy: A company's dividend policy can affect its ROE. If a company retains a significant portion of its earnings for reinvestment, it can potentially generate higher future profits and ROE. Conversely, if a company distributes most of its earnings as dividends, it may have less capital for reinvestment, which could limit future profitability and ROE.

Understanding the interplay of these factors is critical for investors and stakeholders. It underscores the importance of a holistic approach to financial analysis, where ROE is considered alongside other financial metrics, enabling a comprehensive evaluation of a company's performance.

The capital employed in a business also significantly impacts ROE. A company with a high level of capital employed might see a lower ROE due to a higher equity base, even if it is profitable. On the other hand, a company with low capital employed might achieve a higher ROE, given it has a lower equity base and can generate substantial profits.

Conclusion

Calculating Return on Equity (ROE) is vital for assessing your company's financial health and efficiency. ROE measures how effectively your company generates net profit per dollar of shareholders' equity. To calculate ROE, divide net income by average shareholders' equity.

A higher ROE suggests efficient capital use. However, consider it alongside industry benchmarks and trends. ROE can be affected by management decisions like stock buybacks. Tracking ROE over time reveals consistency or areas for improvement.

Remember, ROE is just one metric; assess it alongside related metrics like ROA, profit margin, asset turnover, financial leverage, and the DuPont formula for a comprehensive evaluation and informed decision-making.

FAQ

Q: What is the return on equity (ROE)?

A: Return on Equity (ROE) is a financial ratio that measures the net profit generated by a company based on each dollar of equity investment contributed by shareholders. It measures how efficiently a company uses its equity capital to generate net income.

Q: How is the return on equity calculated?

A: Return on equity is calculated by dividing the net income of a company by its average shareholders' equity and multiplying the result by 100 to express it as a percentage.

Q: What does a higher ROE indicate?

A: A higher ROE indicates that the company is more efficient in generating profits with the equity capital provided by its shareholders.

Q: Can ROE be used as a standalone metric?

A: ROE should not be used as a standalone metric and should be considered in conjunction with other factors to get a clearer picture of a company's performance.

Q: Can the ROE ratio vary across industries?

A: Yes, the ROE ratio can vary across industries, so it is essential to compare a company's ROE to its peers in the same sector to assess its performance.

Q: What factors can impact ROE?

A: ROE can be impacted by discretionary management decisions, such as stock buybacks or dividends issuance, as well as other factors, such as industry dynamics and one-time events.

Q: How should ROE be analyzed?

A: ROE should be analyzed over some time to assess a company's consistent performance.

Q: Are there other financial metrics related to ROE?

A: Yes, other related financial metrics include return on assets (ROA), profit margin, asset turnover, financial leverage, and the DuPont formula.

Q: How can ROE be used to evaluate financial performance?

A: ROE can help investors evaluate a company's financial performance, efficiency, and ability to generate profits for shareholders.