Your Complete Guide to General Ledger Reconciliation

General ledger reconciliation is essential to maintaining accurate financial records for any business. As the central repository of financial transactions, the general ledger plays a critical role in this process.

Regular reconciliations are necessary to ensure the accuracy and integrity of the general ledger. However, doing so manually is time-consuming and prone to error and risk Let’s look at what a general ledger reconciliation is, why it’s important, and how automation helps make it much easier to do regularly.

A general ledger is the central repository of all financial transactions within an organisation. It includes various accounts that track assets, liabilities, equity, revenue, and expenses.

A general ledger can be divided into sub-ledgers to track detailed information about specific types of transactions, such as accounts receivable, accounts payable, and fixed assets.

What is a General Ledger?

The general ledger is the foundation of a business's accounting system. It provides a detailed record of all financial transactions, which can be used to prepare financial statements, track financial performance, and make informed business decisions.

Here are some specific uses of the general ledger:

- To prepare financial statements, such as the balance sheet, income statement, and statement of cash flows.

- To track the financial performance of a business over time.

- To identify trends and areas where improvement is needed.

- To make informed business decisions, such as investing in new equipment or expanding into new markets.

- To comply with accounting regulations.

The general ledger is a valuable tool for businesses of all sizes. By keeping accurate and up-to-date records in the general ledger, companies can improve their financial health and make better decisions about their future.

What is General Ledger Reconciliation?

General ledger reconciliation is a method where accountants validate the completeness and accuracy of account balances in a firm's general ledger.

It involves comparing the account balances in the general ledger with supporting documentation, such as bank statements, invoices, receipts, and other financial records.

Reconciliation aims to identify and correct any errors or discrepancies in the general ledger. This helps to ensure that the general ledger is an accurate and reliable record of the organisation's financial transactions.

Reconciliation is an important part of maintaining financial integrity and ensuring the organisation meets its compliance requirements. It also helps identify areas where the organisation can improve its financial reporting and internal controls.

Types of General Ledger Reconciliations

General ledger reconciliation is a crucial part of any business's financial health, ensuring that the figures in the general ledger accurately reflect all transactions. Understanding the different types of general ledger reconciliations can help businesses choose the most effective method for their needs. Here’s an overview of the most common reconciliation methods:

Bank Reconciliations

This type involves comparing the company's recorded transactions in the general ledger against bank statements or other financial reports from third parties like credit card companies and loan providers. It ensures all banking activities are accurately captured in the company’s financial records.

Customer Reconciliation

Here, a business verifies its account receivables by comparing invoiced amounts to what’s recorded in the general ledger. This may also include reaching out to customers for confirmation of their recorded balances, enhancing the accuracy of receivables.

Vendor Reconciliations

This process requires businesses to match their accounts payable with the statements or invoices received from suppliers. Ensuring these figures align helps maintain accurate payable accounts and fosters healthy vendor relationships.

Account Variance Analysis

For accounts lacking external validation reports (like many expense accounts), businesses can compare the start and end balances, analysing variances to confirm accuracy. This method relies on internal data, examining the monthly activity against the variance to ensure correctness.

Each reconciliation type serves a unique purpose, addressing different aspects of a business's financial activities. Businesses should select the approach that best suits their operational needs, ensuring consistent application for optimal financial clarity and control. Additionally, leveraging account reconciliation software can automate significant portions of these processes, allowing businesses to focus on analysing discrepancies and making strategic decisions. Regardless of the method chosen, regular and diligent general ledger reconciliation is essential for maintaining accurate financial statements and supporting effective business management.

How do you Perform a General Ledger Reconciliation?

The process of preparing a general ledger account reconciliation involves several steps to ensure accuracy and completeness. It may vary depending on the complexity of the organisation and the specific accounts being reconciled.

Here is a step-by-step guide that can serve as a template to follow:

Step 1: Gather Supporting Documentation

Collect all relevant financial records, including bank statements, invoices, receipts, and other supporting documents that provide evidence of financial transactions. These documents will serve as a basis for comparing and reconciling the account balances in the general ledger.

Step 2: Identify Reconciliation Items

Review each account in the general ledger and identify the corresponding items that need to be reconciled. This may include bank accounts, accounts receivable, accounts payable, inventory, and other balance sheet or income statement accounts.

Step 3: Compare Account Balances

Compare the account balances in the general ledger with those reflected in the supporting documentation. This step helps identify discrepancies between the recorded amounts and the actual transactions.

Step 4: Investigate and Resolve Differences

If discrepancies are found during the comparison, investigate the reasons behind the differences. This may involve reviewing transaction records, contacting relevant parties, or performing additional analysis. Once the cause of the discrepancy is identified, could you take the necessary steps to resolve it? This could involve adjusting the general ledger, correcting errors, or seeking clarification from external parties.

Step 5: Update the General Ledger

After resolving the discrepancies, update the general ledger to reflect the corrected account balances. Make the necessary adjustments and ensure that all transactions are accurately recorded in the appropriate accounts.

Step 6: Document the Reconciliation Process

Maintain a record of the reconciliation process, including the steps followed, the discrepancies identified, and the actions taken to resolve them. This documentation serves as a reference for future audits, reviews, and internal control purposes.

Step 7: Review and Approve

Once the reconciliation is complete, review the results and obtain appropriate approvals from relevant stakeholders, such as management or finance teams. This step ensures that the reconciliation is accurate and reliable.

By following these steps, organizations can effectively prepare general ledger account reconciliations and ensure the accuracy and integrity of their financial records.

Benefits of General Ledger Reconciliation

General ledger reconciliation offers several benefits to organisations, ensuring the accuracy and integrity of financial records, improved decision-making, and increased compliance.

Here are some key advantages:

- Identify Errors and Discrepancies: By comparing the balances in the general ledger with supporting documentation, general ledger reconciliation helps detect errors, omissions, or discrepancies in financial records. This allows for prompt resolution and prevents the accumulation of inaccuracies over time.

- Ensure Financial Accuracy: Reconciling the general ledger helps ensure the recorded account balances accurately reflect the actual financial transactions. It provides confidence in the financial statements and supports the integrity of the organisation's financial reporting.

- Improve Internal Controls: General ledger reconciliation is an essential control mechanism that helps identify weaknesses or gaps in internal processes. It allows organisations to implement corrective measures and strengthen their internal control environment, reducing the risk of fraud, errors, and misstatements.

- Facilitate Decision-Making: Accurate and up-to-date financial information is crucial for making informed business decisions. General ledger reconciliation provides reliable data, enabling management to analyse financial performance, assess profitability, and evaluate the organisation's financial health.

- Enhance Audit Readiness: Regular general ledger reconciliation ensures that financial records are well-maintained and supported by appropriate documentation. This facilitates the audit process by providing auditors with organised and reliable information, reducing audit time and potential audit findings.

- Compliance with Regulations and Standards: Many industries and jurisdictions have specific regulatory requirements and accounting standards that organisations must adhere to. General ledger reconciliation helps ensure compliance with these regulations, providing transparency and accountability in financial reporting.

- Streamline Financial Operations: Effective general ledger reconciliation streamlines financial operations by identifying inefficiencies, redundant processes, and areas for improvement. Organisations can optimise their financial processes and improve overall efficiency by resolving discrepancies and enhancing accuracy.

- Establish Trust and Confidence: Accurate financial records and transparent reporting build trust and confidence among stakeholders, including investors, lenders, customers, and business partners. General ledger reconciliation demonstrates a commitment to financial integrity, strengthening relationships and reputation.

Examples of General Ledger Account Reconciliation

General ledger account reconciliation is a crucial process that ensures the accuracy and integrity of financial records. Here are some common examples of general ledger account reconciliation:

1. Bank Reconciliation:

Bank reconciliation involves comparing the transactions recorded in the company's accounting records with those listed on the bank statement. Discrepancies between the two sources are identified and resolved to ensure that the company's cash balances are accurate.

Process:

- Compare the bank statement balance with the general ledger cash account balance.

- Identify and record any outstanding checks or deposits in transit.

- Reconcile bank service charges, interest earned, and other fees.

- Adjust the general ledger balance to match the bank statement balance.

2. Credit Card Reconciliation:

Credit card reconciliation involves reconciling credit card transactions recorded in the general ledger with those listed on the credit card statement. This process ensures that all credit card expenses are accurately recorded and accounted for.

Process:

- Compare credit card transactions recorded in the general ledger with transactions listed on the credit card statement.

- Identify and record any discrepancies, such as missing or duplicate transactions.

- Reconcile any outstanding credit card payments or refunds.

- Adjust the general ledger balance to match the credit card statement balance.

3. Vendor Reconciliation:

Vendor reconciliation involves reconciling accounts payable transactions recorded in the general ledger with those recorded by the company's vendors. This process ensures that all vendor invoices are accurately recorded and that any discrepancies are resolved promptly.

Process:

- Compare accounts payable transactions recorded in the general ledger with vendor invoices and statements.

- Identify and resolve any discrepancies, such as incorrect invoice amounts or missing invoices.

- Reconcile any outstanding vendor payments or credits.

- Adjust the general ledger balance to match the vendor account balances.

4. Accounts Receivable Reconciliation:

Accounts receivable reconciliation involves reconciling customer payments recorded in the general ledger with payments received from customers. This process ensures that all customer payments are accurately recorded and that any discrepancies are resolved promptly.

Process:

- Compare accounts receivable transactions recorded in the general ledger with customer payments received.

- Identify and resolve any discrepancies, such as incorrect payment amounts or missing payments.

- Reconcile any outstanding customer invoices or credits.

- Adjust the general ledger balance to match the accounts receivable account balances.

5. Intercompany Reconciliation:

Intercompany reconciliation involves reconciling transactions between different entities within the same organisation. This process ensures that transactions between intercompany accounts are accurately recorded and eliminate any discrepancies.

Process:

- Compare intercompany transactions recorded in the general ledger of each entity.

- Identify and resolve any discrepancies, such as misclassified transactions or missing entries.

- Reconcile any intercompany balances or transactions.

- Adjust the general ledger balances of each entity to ensure consistency and accuracy.

These are just a few examples of general ledger account reconciliation processes. Each type of reconciliation plays a vital role in maintaining accurate financial records and ensuring compliance with accounting standards and regulations.

Common Errors in the Manual General Ledger Reconciliation Process

General ledger reconciliation is a critical process for ensuring the accuracy of financial records. However, there are common errors that can occur during the reconciliation process.

By understanding these pitfalls, organizations can enhance the effectiveness of their reconciliation process.

Here are some of the most common errors in general ledger reconciliation:

- Inaccurate data entry: Organizations should implement controls such as double-checking data entry and using automated data capture solutions to prevent these errors.

- Insufficient or missing supporting documentation: Proper documentation is essential for accurate reconciliation. Organizations should ensure that all supporting documentation is filed correctly and accessible.

- Infrequent reconciliations: Regular reconciliations are essential for accurate financial records. Delayed or irregular reconciliations can lead to a buildup of errors and discrepancies.

- Lack of proper review and approval processes: Errors can go unnoticed or unaddressed if no adequate review and approval processes exist.

- Poor communication and collaboration: Poor communication and collaboration between teams involved in the reconciliation process can lead to errors and delays.

- Manual reconciliation processes: Manual reconciliation is prone to errors and can be time-consuming. Organizations should use automated reconciliation solutions to streamline the process and improve accuracy.

- Unstandardized reconciliation methodologies: Unstandardized reconciliation methods can lead to inconsistencies. Standardize procedures to ensure consistency and accuracy.

By being aware of these common errors and implementing adequate controls and best practices, organizations can enhance the accuracy and efficiency of their general ledger reconciliation process.

Why you should Automate General Ledger Reconciliation

Automating the general ledger reconciliation process brings a transformative shift to accounting practices, significantly enhancing efficiency and accuracy. The traditional method, characterised by its time-intensive nature due to the dispersion of data across various systems, often results in a laborious and error-prone process. However, the advent of automation technology presents a streamlined solution.

By integrating automated reconciliation software, accountants can effortlessly import necessary data from diverse sources, including ERP systems, bank and credit statements, and the general ledger itself, alongside other third-party platforms. This technology not only facilitates the automatic comparison and verification of data across these sources but also promptly identifies and flags discrepancies for review. As a result, this reduces the manual workload, allowing finance teams to allocate their time to more strategic tasks rather than painstakingly combing through data line by line.

Moreover, automated reconciliation tools, such as those offered by advanced platforms, provide comprehensive features from importing and securely storing financial data to generating audit trails and customised financial reports. This level of automation ensures a more accurate, efficient, and reliable reconciliation process, ultimately empowering accountants to focus on value-added activities and strategic financial analysis, thereby reinforcing the financial integrity of the organisation.

Here are some more ways that automation streamlines general ledger reconciliation:

- Eliminate manual data entry: Automated reconciliation solutions can eliminate the need for manual data entry by extracting data from documents and matching it to the general ledger. This can help to reduce errors and improve efficiency.

- Identify and resolve discrepancies: Automated reconciliation solutions can identify discrepancies between the general ledger and supporting documentation. This can help to resolve issues promptly and prevent them from becoming more significant problems.

- Provide real-time insights: Automated reconciliation solutions can provide real-time insights into the financial data. Manual reconciliation can help identify trends and patterns that may not be visible.

- Improve compliance: Automated reconciliation solutions can help organisations to comply with financial regulations. This is because they can help ensure the general ledger is accurate and complete.

Automation is an excellent option if you want to streamline your general ledger reconciliation process.

Looking out for a Reconciliation Software?

Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

General Ledger Reconciliation Automation with Nanonets

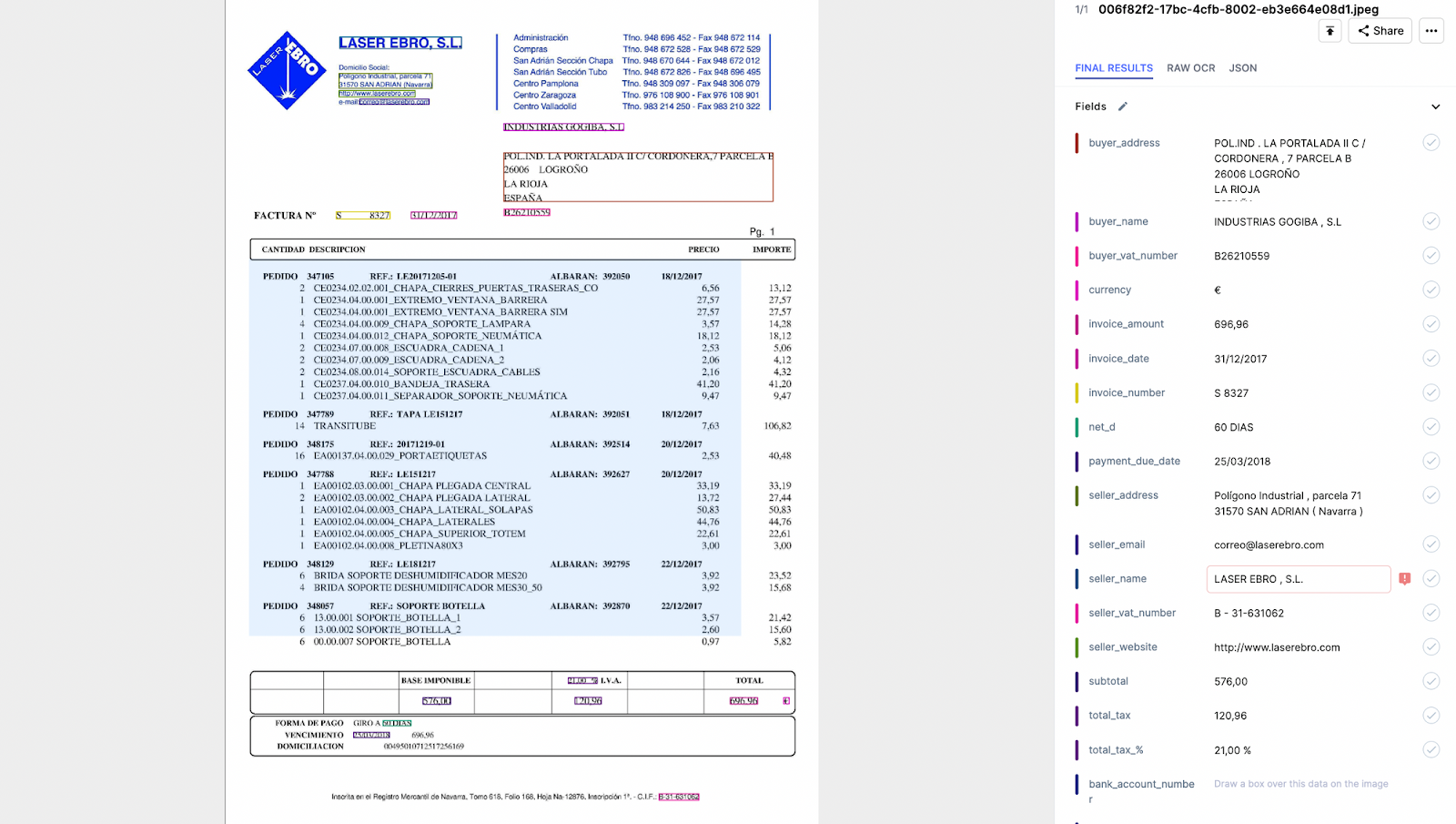

Nanonets offers advanced automation solutions that can streamline and enhance the general ledger reconciliation process. It uses AI-powered OCR technology to extract relevant information from financial documents and statements, eliminating the need for manual data entry and reducing the risk of errors.

Nanonets also uses intelligent algorithms to match extracted data with corresponding entries in the general ledger, identifying discrepancies and highlighting potential errors or missing entries. This automated matching and reconciliation process ensures accuracy and minimizes the risk of human error.

With Nanonets, organizations gain real-time visibility into the reconciliation process. Comprehensive reports and analytics provide insights into the status of reconciliations, highlighting key metrics and trends. This helps finance teams identify bottlenecks, track performance, and make data-driven decisions to improve their general ledger reconciliation process.

By leveraging the power of automation with Nanonets, businesses can achieve faster, more accurate, and more efficient general ledger reconciliation. The advanced capabilities of Nanonets free up valuable time for finance teams, allowing them to focus on strategic analysis, exception handling, and other value-added activities.

FAQs

What is general ledger reconciliation?

General ledger reconciliation is the process of verifying the accuracy and consistency of account balances in the general ledger.

Why do we do general ledger reconciliation?

General ledger reconciliation is performed to ensure the accuracy and integrity of financial records.

What is the difference between a balance sheet and a general ledger?

A balance sheet is a snapshot of a company's financial position at a specific point in time, while a general ledger is a detailed record of all financial transactions that have occurred over a period of time.

What is the difference between bank reconciliation and general ledger?

Bank reconciliation compares the bank statement to the general ledger, while the general ledger is a record of all financial transactions.

What are the 4 primary components of the general ledger?

The four primary components of the general ledger are assets, liabilities, equity, and revenues/expenses.

How do you reconcile a general ledger with a bank statement?

Reconciling a general ledger with a bank statement involves comparing the transactions recorded in the general ledger with the transactions listed in the bank statement.

What is a practical example of general ledger reconciliation?

A practical example of general ledger reconciliation is comparing the balance in a company's bank account with the balance shown on the bank statement.

How can automation streamline general ledger reconciliation?

Automation can streamline general ledger reconciliation by eliminating manual tasks and reducing the risk of errors.