What is a Bank Remittance?

A Bank remittance is a payment sent from one bank account to another, commonly across borders, for transactions like purchases. It can be used for bill payments, invoices, or transferring money to friends and family. This transfer occurs through various means, including electronic payment systems, wire transfers, mail, drafts, or checks.

Sending a bank remittance is typically faster and more convenient than sending a check or money order through the mail. In addition, bank remittances can be tracked so that the sender can confirm that the money was received by the intended recipient.

Most banks offer online tools that allow customers to easily send bank remittances. Customers typically need to log into their online banking account and then provide the required information about the recipient and the amount of the payment. Once the payment is processed, the sender will receive a confirmation number that can be used to track the status of the payment.

How Does Bank Remittance Work?

Bank remittance can be done online, through a mobile app, or in person at a physical bank branch. The sender will need to provide the recipient's bank account number and routing number, as well as the amount of the payment. Once the payment is processed, the sender will receive a confirmation number that can be used to track the status of the payment. Remittance is a 6 step process:

- Initiation: The sender provides details of the recipient to their bank like transfer amount and recipient bank details

- Authorization: The orignating bank verifies the sender's details and checks if the sender has sufficient funds in their account to cover the transfer.

- Processing: Once the sender's bank has verified the transaction details, it processes the remittance. This may involve using various payment systems and networks, depending on the type of transfer and its destination.

In domestic remittances, the process is typically faster and may involve using the country's domestic payment infrastructure, such as the Automated Clearing House (ACH) in the United States.

In international remittances, the process can be more complex and may involve multiple banks and payment intermediaries, especially if currency conversion is required. - Funds Transfer: The sender's bank deducts the specified amount from the sender's account. The recipient's bank then credits the funds to the recipient's account.

The sender and the recipient receive notifications confirming the completion of the remittance.

Note: In international remittances, additional fees may be charged by the banks and intermediaries involved in the process. These fees can include transaction fees, currency conversion fees, and service charges. It's essential for both the sender and the recipient to be aware of any fees and exchange rates that may affect the remittance.

What is the Difference Between a Bank Remittance and a Bank Transfer?

A bank transfer typically involves moving money from one account to another within the same bank or between accounts at different banks. This can be done electronically or through other means, and it's a common way to send money domestically or internationally.

On the other hand, a bank remittance specifically refers to the transfer of money from one individual or entity to another, often across borders. It may involve a transfer between different banks or financial institutions, and it's commonly associated with international money transfers, particularly those involving migrant workers sending money back to their home countries.

In summary, while both bank transfers and bank remittances involve moving money between accounts, a bank remittance specifically refers to cross-border transfers, whereas bank transfers can encompass a wider range of transactions, including domestic transfers.

Advantages of Using Bank Remittance

There are several advantages of using a bank remittance:

- Speed: When you use a bank remittance, the money is typically deposited into your account within one to two days. This is much faster than if you were to wait for the customer to send you a check or money order, which can take weeks to arrive.

- Security: When you use a bank remittance, the money is transferred using a secure network. This means that there is less risk of the money being lost or stolen en route.

- Accuracy: When you use a bank remittance, the exchange rate is set in advance. This means that you will know exactly how much money will be deposited into your account, without having to worry about the fluctuating exchange rate.

- Convenience: When you use a bank remittance, you don't have to worry about dealing with different currencies. The bank will handle the conversion for you, so you can focus on running your business.

If you frequently receive payments from customers in other countries, using a bank remittance can be a convenient and efficient way to manage your finances.

What Are the Costs of Bank Remittance?

There are some costs associated with bank remittance. The costs can vary from $0 to $50 based on size of transfer, country and intermediaries banks required to complete the transaction.

The fee can be charged both by the sender bank and recipient ban. There may be an exchange rate fee if the sender and recipient have different currencies. This fee will be charged by the recipient's bank and will be based on the current exchange rate between the two currencies.

Risks of Bank Remittance and how to avoid them?

There are a few risks while sending a remittance:

- If the recipient's bank account information is entered incorrectly, the funds may be sent to the wrong account and it would be hard to recover.

- If the sender does not have enough funds in their account to cover the payment, their bank may charge them an overdraft fee. Third, if either bank experiences technical difficulties, the payment may be delayed or cancelled.

How to avoid them:

- Make sure you enter the recipient's bank account information correctly.

- Check with your bank to see if there are any limits on how much money you can send via bank remittance.

- Choose a reputable bank with a good track record of reliability.

Now that you know how bank remittance works and what to consider, you can decide if it is right for you. If you need to send money quickly and securely, bank remittance may be a good option.

Comparing Bank Remittance Services

When you need to send money to family or friends abroad, you have a few options available. You can use a bank’s wire transfer service, an international money transfer service like Western Union or MoneyGram, or you can send a remittance. But what’s the difference between these services, and which one is the best option for you?

If you have a bank account, you can usually send a wire transfer directly from your bank’s website or mobile app. To do this, you’ll need the recipient’s bank account details, including the bank’s SWIFT code. Wire transfers can be completed in a matter of minutes, but they’re usually not free – you’ll often be charged a fee by both your bank and the recipient’s bank. And if you’re sending money to a country with a different currency, you may also be charged currency conversion fees.

International money transfer services

There are a number of international money transfer services available, including Western Union and MoneyGram. These services allow you to send money to more than 200 countries around the world. You can generally process your transfer online, by phone or in person at a physical location. The speed of the transfer will depend on the service you use, but it’s usually fairly quick – most transfers are completed within a few hours.

One of the main advantages of using an international money transfer service is that you can send cash to people who don’t have a bank account. The recipient can then pick up the cash at a local agent location. However, these services can be expensive – you’ll often be charged a flat fee plus a percentage of the amount you’re sending.

Remittances

Remittances are usually sent through an international money transfer service or a specialized remittance service.

The main advantage of using a remittance service is that they often have much lower fees than other types of money transfer services. This is because remittances are typically large, regular payments, so the companies that facilitate them can offer lower rates to encourage customers to use their service.

Which option is best for you?

When you’re choosing a money transfer method, there are a few things to consider:

How much money are you sending? If you’re sending a large amount of money, a wire transfer from your bank may be the best option as it will usually have lower fees than an international money transfer service.

How quickly do you need the money to be received? If you need the money to be received instantly, an international money transfer service is generally the best option. However, if you can wait a few days for the money to be received, a remittance service may be a better option as they usually have lower fees.

What country are you sending the money to? Some countries have restrictions on how much money can be sent in or out of the country. If you’re sending money to a country with strict regulations, you may need to use a specialized remittance service.

When you’re comparing bank remittance services, it’s important to compare the fees and exchange rates offered by each provider. You should also consider how quickly you need the money to be received, and whether you need to send cash or bank account funds. Another factor you should consider is automation of payments:

Automate Payments

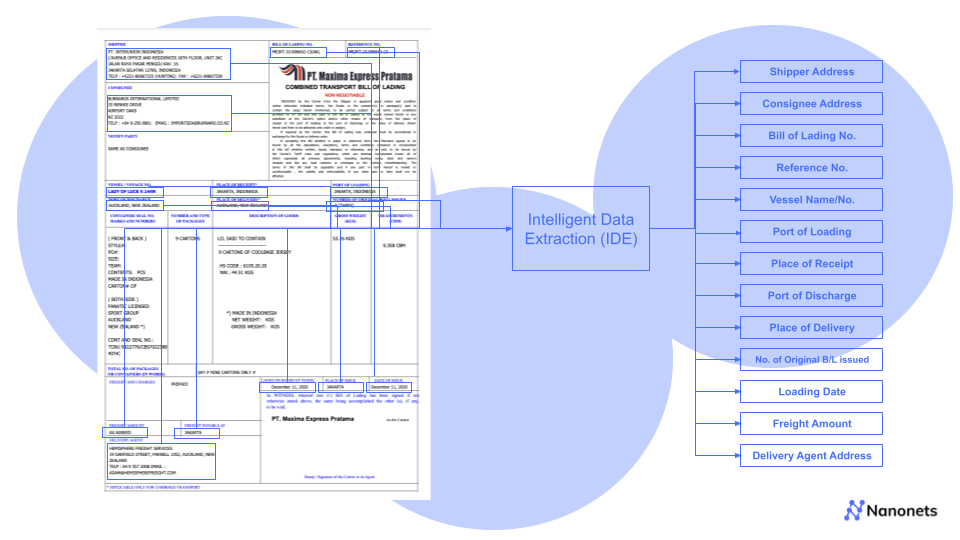

Automation is easy with software like Flow Nanonets which can handle the end-to-end accounts payable process and help you 10x your efficiency. You can automate your invoices, approval, and payment process. Sync data in real-time with your ERP like Quickbooks for reconcilliation, monitoring and performing analytics on your AP process.

With Payment options like ACH & Wire transfer, you can automate your payments without a hassle. To lear more, schedule a call with us:

Regulations Around Bank Remittance

When sending or receiving a bank remittance, it’s important to know the regulations in order to avoid any costly penalties or delays. Depending on the amount of money being remitted and the destination country, there may be different forms that need to be filled out and different documentation that is required.

When sending money abroad, you will need to provide the recipient’s bank account number and routing number, as well as your own account number and routing number. The routing number is a nine digit number that is unique to the bank and is used to identify it when sending or receiving payments. The account number is the number assigned to your specific account at the bank.

If you are receiving a bank remittance, you will need to provide the sender with your account number and routing number. You will also need to have a valid government-issued ID in order to pick up the money.

There are limits on how much money can be sent through a bank remittance. For example, in the United States, the limit is $10,000 per day. If you are sending or receiving a bank remittance that is over the limit, you will need to fill out a form called a Currency Transaction Report (CTR). The CTR is a form that is used to report any transaction over $10,000 that is made in cash, checks, money orders, or traveler’s checks.

Bank remittances are a convenient way to send or receive money, but it’s important to be aware of the regulations before completing a transaction. By knowing the requirements ahead of time, you can avoid any costly penalties or delays.

Summary

A remittance is a transfer of money, either to an individual or to a business. The most common type of remittance is a wire transfer, which is a transfer of funds from one bank account to another. Other types of remittances include electronic funds transfers, which are transfers of funds between two electronic accounts, and check 21 remittances, which are transfers of funds between two banks using the Check 21 system.

There are many reasons why people use remittances. The most common reason is to make a payment for goods or services. Other reasons include sending money to family or friends, transferring money between accounts, or paying bills.

There are many benefits of using remittances. First, they are fast and convenient. Second, they are safe and secure. Third, they are typically less expensive than other methods of payment, such as checks or money orders. Fourth, they can be used to send money to people in other countries.

There are some risks associated with using remittances. First, if the recipient's bank account is in a different country, there may be fees associated with the transfer. Second, the exchange rate may fluctuate, which could result in the recipient receiving less money than was originally sent. Third, the sender may not have the recipient's bank account information, which could delay or prevent the transfer.