How to make ACH payments

What are ACH payments?

ACH (Automated Clearing House) payments are EFTs (electronic fund transfers) that use the ACH network to move funds between bank accounts in the United States. This payment method is widely used for direct deposit of payroll, payment of bills, and business-to-business payments.

The ACH network is managed by NACHA, which was earlier known as the National Automated Clearing House Association. NACHA is a non-profit organization that is responsible for the supervising and rule-making functions for ACH transactions. All ACH transfers are processed through the centralized ACH network operated by NACHA, ensuring secure and accurate transfer of funds to the intended bank account.

ACH payments are quicker and more dependable than traditional paper checks, thereby making accounts payable processes faster. It is crucial to remember that ACH is a separate network from major credit card systems such as Visa, Mastercard, and American Express.

ACH payment requirements

To make an ACH payment, you will need to provide

- The recipient's name

- The type of bank account the recipient has

- The recipient’s bank account number and ABA routing number

- The payment amount

You also need to authorize the payment, which can be done electronically through online banking or by signing a paper authorization form. To ensure a successful ACH payment, you must have a valid bank account, sufficient funds, and accurate information for the recipient's bank account.

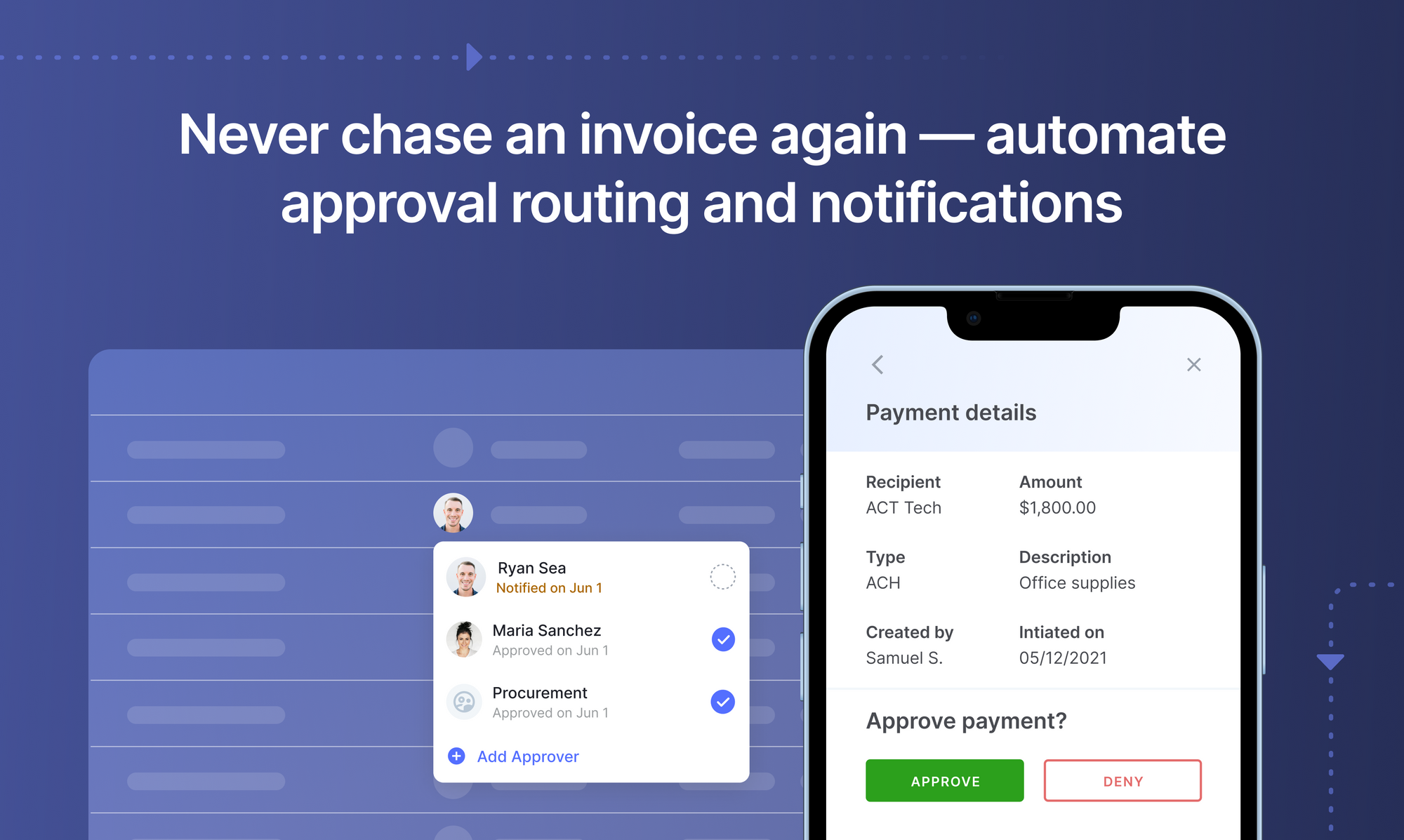

Looking to automate your manual AP process? Book a 30-min live demo to see how Nanonets can help your team implement end-to-end AP automation.

ACH payment examples

Some examples of typical ACH payments are:

- Direct deposit from employers (for things like paychecks)

- Paying bills with your bank account

- Transferring funds from one bank account to another

- Sending money to the IRS

- Businesses paying their vendors and suppliers

There are two types of ACH transfers: ACH credits and ACH debits.

The key difference between the two is that an ACH credit is the money that’s delivered into an account, while an ACH debit is the money that’s pulled out of an account.

In this post, we cover some of these examples and go into more detail on how ACH payments actually work, their benefits and how you can get started.

How long does it take to process an ACH payment?

Although ACH transfers are reasonably fast, they are not instantaneous, and it usually takes 3-5 business days for the funds to be transferred. The time of day and day of the week also affect the transfer time, as well as the type of ACH payment. There are also Next Day ACH transfers and Same Day ACH transfers available.

Next Day ACH transfers typically settle within 1-2 business days, while Same Day ACH transfers can be completed on the same business day or the following business day, depending on when the payment was initiated. However, Same Day ACH transfers usually come with an additional processing fee for the same-day service.

Set up seamless ACH payment and streamline the Accounts Payable process in seconds. Book a 30-min live demo now.

How much do ACH payments cost?

The National Automated Clearing House Association (NACHA), the governing body of ACH payments and transfers, states that the average processing fee for an ACH payment is around 11 cents. However, several factors can affect the cost per transaction.

The volume of transactions being processed is one such factor, with larger transaction volumes resulting in lower per-transaction fees. This is due to the availability of different fee structures that can be used.

How to set up ACH payments

When starting the process of making ACH payments for your organization, it is important to familiarize yourself with a few (necessary) regulations. These are:

- Verification of account information – You must verify that your account information is accurate with the ACH network. This can be achieved by dispatching micro-deposits (typically ranging from 0.01¢ to 0.99¢) to another bank account, which, upon receipt acknowledgment, verifies that your account is properly linked and funded. These deposits will then be refunded to you. You can use a validation tool offered by NACHA or any third-party tool.

- NACHA certification – This certification serves as a trust signal to your customers, indicating that your business adheres to the rules of the ACH network. Note that this certification is intended for third-party operators who handle the transactions, not your business. It is, however, better to select an operator with this certification. For further information, refer to the NACHA website.

- Guidelines for same-day ACH – The rising usage of ACH has resulted in a same-day payment alternative (which is pretty fast as far as business payments are concerned!). This option enables recipients to gain access to their funds at 1 PM local time, provided that the payment was processed that morning.

Getting started with ACH payments

Nanonets provides completely out-of-the-box solutions to get small businesses started with ACH payments at a very reasonable cost. Using partnerships with third party ACH service providers such as Dwolla and Plaid, Nanonets is able to grant access to the ACH network for all major US banks, and allows users to carry out payments at a very low fees of $0.2 per transaction (irrespective of transaction value).

Set up seamless ACH payment and streamline the Accounts Payable process in seconds. Book a 30-min live demo now.