Why "Buy Now Pay Later" is the new Sales Mantra

The pandemic and the associated financial distress have resulted in a recent upsurge in the Buy-Now-Pay-Later (BNPL) scheme of purchase. As the name suggests, BNPL is a form of short-term loans, often interest-free, but sometimes with hidden costs, that allows consumers to make purchases and pay for them at a future date. These are a type of point-of-sale installment (or ‘instalment’ depending on the side of the Atlantic Ocean to which you belong) payment schemes that are increasingly becoming popular options, in both online and offline retail spaces.

Let us learn about what BNPL is, how vendors can use and benefit from it, and the fit of Nanonets in the scene.

Table of Content

- The evolution of BNPL

- The workings of BNPL

- The use of OCR in the BNPL ecosystem

- OCR Extraction of data from unstructured documents

- Advantages of OCR in the BNPL ecosystem

- AI based OCR with Nanonets

- Takeaway

The evolution of BNPL

Paying for purchases in installments is not a new concept. Reportedly developed in the 1850s, the earliest available record of installment-based buying in modern history dates back to the 1920s. The mismatch between the large production capacity in the manufacturing sector and consumer demand during the post WW-1 depression period resulted in the extensive use of installment plans both in the US and elsewhere in the world.

If recession and associated thrift drove the installment model in the 1920s, the scheme has continued to exist across the century. Prior to the recent pandemic induced economic downturn, installment schemes contributed to 1% of sales in the US alone, driven partly by economic needs and partly by the instant-gratification-deferred-payment style of modern life.

Buy-Now-Pay-Later is simply old wine in a new bottle. With third-party BNPL providers such as Klarna, Affirm etc., interfacing between merchants and consumers, this type of payment option has gained ground in recent years. The recent pandemic-induced economic downturn has further enhanced the reach and spread of this form of payment in the retail space.

The workings of BNPL

For the consumer

BNPL is increasingly being used both in the online and offline marketplace.

- In the online platform, when the customer chooses her product and prepares to make an online purchase, if the marketplace has the option of BNPL, she would be taken to a site that provides the option of deferred payment such as that shown below.

- If the customer chooses the interest-free payment through the BNPL app, she is asked for details, which may include credit and bank details by the BNPL enabler.

- In the offline store, the customer fills out a form manually with details or communicates the data to the employee of the store. The details are then entered into a digital database by a clerk or verbally communicates with a clerk who enters the data into a digital form. In some stores, a tablet/electronic pad is provided to the customer into which she fills the data required.

- The details are checked by the merchant or a third-party provider for validity and approval.

- If approved, a small down payment, such as 25% of the overall purchase amount may be required, with subsequent payments to be paid at a later specified time in a series of interest-free installments.

- All installments may be paid by check or bank transfer; or automatically debited from a debit card, bank account, or credit card.

- The difference between BNPL payment and credit card payment is that the former is often interest-free (but not always), and the purchase is paid off completely during the stipulated period. In credit cards, the credit may be extended indefinitely, with interest accruing with increased times.

For the merchant

Merchants looking to adopt a BNPL solution could either set up such a system themselves (merchant model using finance technician or FinTech) or avail of a third-party BNPL provider (partner model).

The Merchant Model is straightforward; the merchant enters into an agreement with the customer to plan the payment of the goods purchased over many installments. There may or may not be an interest added to the payment method, depending on the merchant’s policies, the value of the goods sold, and the duration of the installment.

For the BNPL provider

In the partner model, a third-party interfaces between the merchant and the customer and offers the installment payment option. There are two types of third-party BNPL solutions – merchant transaction fee loans and shopper interest loans:

In merchant transaction fee type BNPL, the customer is not charged any extra amount for availing of the option of BNPL. Instead, the merchant is charged a fee that is typically 2-8% of the purchase amount.

In shopper interest loans, the merchant is not charged a fee, but the customer pays interest as part of their installment plan. This is similar to the traditional installment plans that have existed for more than a century now.

The partner model typically works as follows:

- When the customer chooses the BNPL option of purchase, she is required to provide information about the amounts of each installment, the period over which they are paid, and the mode of payment (credit card, debit card, bank transfer, online banking, etc.).

- The customer is then required to provide appropriate details such as credit card number, bank account number, etc., using which the provider may perform a credit check on the customer.

- Once approved, the purchase is deemed complete.

- Once the purchase process is completed at the customer’s end, the provider pays the full amount of the purchase to the merchant, minus any fees that have been agreed with the merchant.

- The provider collects the remaining installments directly from the customer at the predetermined time periods.

The use of OCR in the BNPL ecosystem

OCR is useful in two steps of the BNPL protocol, viz., at the data entry step and at the stage of KYC verification by the BNPL provider.

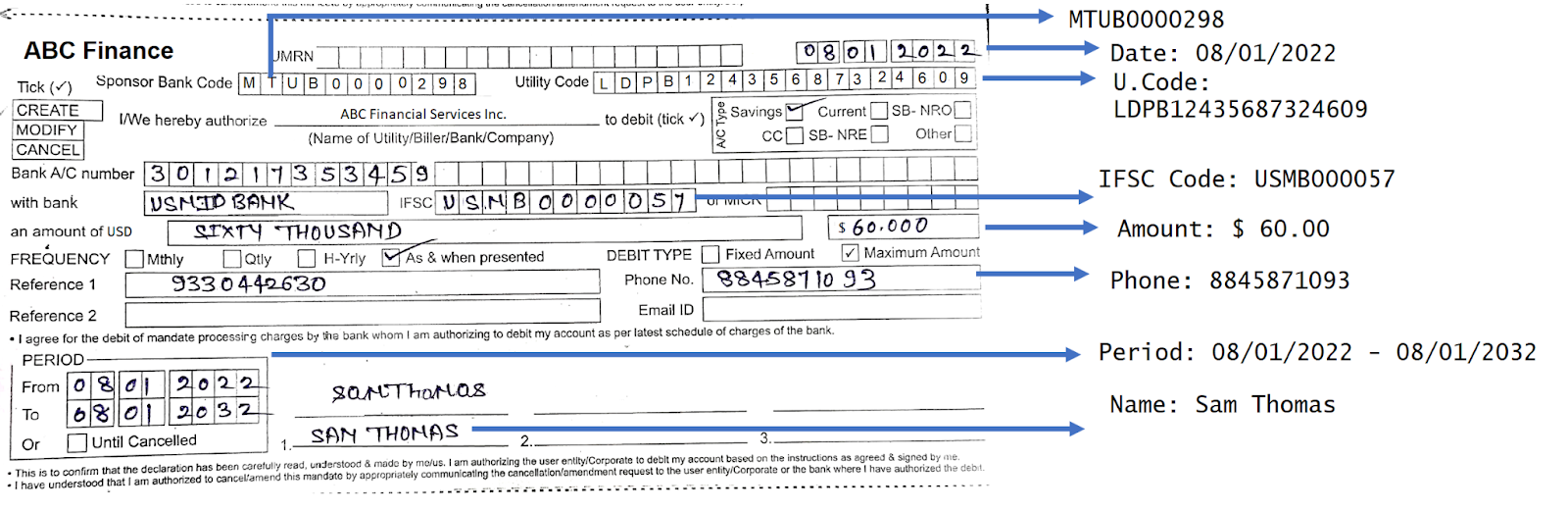

In the offline store that chooses to use BNPL, the customer is often required to fill out a form with details that must be entered into the computer. Oftentimes the form is something like this:

The data filled out by the customer on the form must be manually entered into a system by an employee into a database. The BNPL software then validates the data and sends back the approval note for further processing. This is like the credit card being swiped and the data being validated for approval.

The BNPL service provider can also enormously benefit from the use of OCR in checking the attached KYC documents such as the ID, bank details etc. These KYC checks must happen in real-time and automatic data extraction from the uploaded documents will help in the quick verification of relevant data from these documents with source information.

Manual entry of financial data for BNPL operations has the following problems:

1. High Error Rates: Raw Data entry not followed by verification steps has been shown to have an error rate as high as 4%. To put that in perspective, there are 2 errors for every five entries made. Any error in finance details can be catastrophic to the organization and the customer. The high error rates associated with manual data entry can be attributed to a variety of reasons, from inadequate training of data entry professionals to human fatigue, misinterpretation of data, etc. According to ‘Data Quality Assessment’, errors can arise from missing values, which can, in turn, create discrepancies in the desired output. Even the best data entry operator is prone to making mistakes when the data entry task is repetitive and/or involves a large volume of data. Or, the companies would have to outsource the data entry operation, which again costs money.

2. Delays: Manual entry of data is time-consuming. A good rate of data entry from paper documents ranges between 10,000 and 15,000 keystrokes per hour. Complex data that require comprehension before being entered, would delay the process further. Thus entering 400 units of data would take a competent operator between 8 and 10 minutes, which becomes unacceptable if the volume of data is high.

3. Human Boredom: The process of manual data entry is repetitive and tedious and can be demoralizing. Manual data entry could thus lead to employee dissatisfaction and a high turnover rate. These are serious problems in today’s highly competitive business environment.

This is where OCR data extraction software can help

Optical Character Recognition or OCR converts any kind of text or information stored in digital documents into machine-readable data. Hard copies and paper documents can thus be converted into computer-readable file formats, suitable for further editing or data processing; facilitating the transition to paperless offices.

OCR Extraction of data from unstructured documents

A good OCR must be able to:

- Extract structured, poorly structured, and unstructured data.

- Pull data from multiple sources.

- Export extracted data in the desired format

- Be integrated with a software that conveys the data in real-time to the FinTech enabler in business or the third party BNPL provider

An ideal way in which the OCR can be used for BNPL processing is when it is directly integrated into FinTech’s pipeline.

Advantages of OCR in the BNPL ecosystem

- Improvement of accuracy and reduction of human errors: Automation can eliminate many of the human errors that are brought about by oversight, fatigue, or inadequate training.

- Time savings: Automation is undoubtedly faster than manual extraction of data. The financial and credit data of the customer must be transmitted to the financial technician in real-time for the purchase process to be completed during this visit. Automated entry of data can hasten the process and thereby avoid delays in the purchase process.

- Better control and access to data: A centralized location of structured data makes it more accessible to all stakeholders and participants in the business, thereby allowing coherence in business activities.

- Cost benefits: While the initial investment in OCR automation can be daunting, the cost savings through productivity improvements, employee morale, and time savings can compensate for the setting up costs of automated data extraction systems.

- Scalability: OCR data extraction systems offer scope for scaling up of the business without worrying about the volumes of data that would correspondingly be scaled.

AI-based OCR with Nanonets

Nanonets is an OCR software that leverages AI & ML capabilities to automatically extract unstructured/structured data from PDF documents, images, and scanned files. Unlike traditional OCR solutions, Nanonets doesn’t require separate rules and templates for each new document type.

Relying on AI-driven cognitive intelligence, Nanonets can handle semi-structured and even unseen document types while improving over time. The Nanonets algorithm & OCR models learn continuously. They can be trained or retrained multiple times and are very customizable. You can also customize the output, to only extract specific tables or data entries of your interest.

The Nanonets API provides high speeds and great accuracy in line item extraction of data and drives automation for line item management. The Nanonets API can perform the following tasks:

- Accurate detection of the table structure of a line item containing documents like forms.

- All the line item entries that are present in the forms like name, product, price, total sum, discounts, etc.

- The data can be extracted as JSON output that can enable the building of customized apps and platforms.

While offering a great API & documentation for developers, the software is also ideal for organizations with no in-house team of developers.

The benefits of using Nanonets over other automated OCR software go far beyond cost savings, accuracy, and scale. Nanonets additionally provides unique benefits that place it far ahead of the competition:

- A truly no-code tool

- Easy integration of Nanonets with most CRM, ERP, content services, or RPA software.

- No post-processing needed: Nanonets OCR can recognize handwritten text, images of text in multiple languages at once, images with low resolution, images with new or cursive fonts and varying sizes, images with shadowy text, tilted text, random unstructured text, image noise, blurred images and more.

- Works with custom data through the use of custom data for training OCR models.

- Multiple input recognition: Nanonets OCR can recognize handwritten text, images of text in multiple languages at once, images with low resolution, images with new or cursive fonts and varying sizes, images with shadowy text, tilted text, random unstructured text, image noise, blurred images, and multiple languages

- Independence from formats: Nanonets is not bound by the template of documents at all. You can capture data cognitively in tables or line items or any other format!

Takeaway

The consumer landscape has changed tremendously in the past 20 years, particularly in the past two years of pandemic-induced lockdowns and economic downturns. From a space that was once reliant on cash purchases to one that’s now fully embracing digitization of transactions, the marketplace is going through a transformation that’s allowing it to harness technology and new innovations to their full potential. The BNPL approach is the next logical step in the evolution of the retail space. The use of OCR in the BNPL workflow comes with compelling benefits such as time and cost savings, streamlined approval process, and ultimately better adoption by merchants